Stablecoin yield: Managing risk during a market downtrend

This post is a guide for earning yield on stablecoins during market downturns.

During downturns in the crypto market, you may see people posting about “being in stables”. This refers to de-risking their portfolio away from volatile assets to something less risky like a stablecoin that they can use to earn a yield while waiting for more favorable market conditions.

If you are new to crypto, it is important to be aware that these yield opportunities mostly reside “on-chain”. This means it is important to be comfortable with self custody of your crypto using Metamask or a hardware wallet. It is also important to be comfortable interacting with the blockchain and making transactions and knowing the risks associated with doing so.

What is a stablecoin?

A stablecoin is a crypto asset that it is meant to have the same price as a real world asset, like the US dollar. Maintaining the equal price to the dollar is called “keeping peg”, an important measure for stablecoins.

Risks of Earning Yield with Stablecoins

When earning yield with stablecoin pools there are two major risks to be aware of.

The first risk involves the viability of the stablecoin project, how established is the platform? Is it centralized or decentralized? (Each has their own set of risks) How well does it keep peg to the asset it is supposed to mirror? What are the risks that would cause the stablecoin to lose value? This became a concern with the rise of algorithmic stablecoins, many of which failed to maintain their peg to the US dollar due to their design.

The second risk to be aware of is the secondary layer you might be using to stake LP (Liquidity Pool) tokens and earn a yield. The security of the project that is issuing rewards (Many decentralized exchanges run rewards programs for stablecoin liquidity providers) or auto compounding (i.e. Beefy Finance) is another layer of counterparty risk and complexity that must be taken into account.

With the platform risk of the stablecoin projects in mind, we will provide a brief overview of the most popular projects.

Centralized vs Decentralized

The biggest distinction between stablecoin projects is their focus on decentralization. Centralization is the norm for traditional companies, decentralization is much more difficult but has different characteristics. A centralized stablecoin like USDC is regulated by the financial system and has all the assurances you would expect from a regulated business. Decentralized stablecoins like DAI typically live on the blockchain and are mostly governed by the code that makes up the protocol. They often use crypto tokens as collateral to back the system instead of traditional methods like backing with cash or low risk debt.

The “Blue Chip” Stablecoins (lower risk)

Ranked by market capitalization, a proxy measure for popularity and trust.

USDT ($80 Billion market cap)

Originally started by Bitfinex, USDT or “Tether” as it is commonly referred to was the first stablecoin to get widely adopted by exchanges, primarily in Asia. Tether is often accused of not showing enough proof that their supply is backed by liquid assets and has been the subject of many stories in the media.

USDC ($50 Billion market cap)

Backed by Circle, USDC is the premiere centralized stablecoin regulated in the United States. One reason for USDC’s popularity is the ease with which USDC can be redeemed for US dollars. It has a long reputation of working with regulators to ensure that reserves are used responsibly and accounted for. Due to its centralized nature, wallet addresses that have been identified by authorities as involved in illegal activity can be blacklisted by Circle, a feature that is common among the centralized stablecoin projects.

DAI ($9 Billion market cap)

Started by the Maker Foundation, DAI is the premiere decentralized stablecoin that is backed with crypto assets rather than being backed by traditional financial instruments or USD cash. DAI has taken some heat recently due to the percentage of the centralized collateral backing it (USDC) and negating some of the value of their decentralization claims.

The Up and Coming Stablecoin Projects (higher risk)

FRAX ($3 billion market cap)

Frax is an algorithmic stablecoin project that has taken a conservative approach to ensure the FRAX stablecoin token maintains peg to the dollar. The assets on Frax’s balance sheet are other stablecoins. Frax is able to adjust its collateralization level according to the demand for its own currency. When there is more demand for FRAX tokens, the system can run looser, and when demand wanes, it can tighten.

An innovative element of Frax is the Algorithmic Market Operations (AMOs). Central banks engage in “Open Market Operations”—creating new currency to directly intervene in the market. Frax is designed to have the same flexibility. Frax allows anyone to propose an AMO strategy via governance (similar to Yearn), and if the strategy is good for the Frax ecosystem, it is free to be adopted.

MIM ($3 billion market cap)

Magic Internet Money (MIM) is the stablecoin for Abracadabra protocol backed by interest-bearing tokens (ibTKNS). ‘ibTKNs’ are used because they accumulate interest and increase in price over time. These tokens increase in volume as users pay back interest on portions they borrowed from the lending pool.

FEI ($500 million market cap)

FEI recently merged with Rari Protocol and FEI is one of the offerings in their suite of DeFi products. The FEI stablecoin has an uncapped supply that tracks demand. FEI enters circulation via sale along a bonding curve. This curve approaches and fixes at the $1 peg. When new demand for FEI arises, users can acquire it by buying on the bonding curve.

MAI ($300 million market cap)

MAI is a stablecoin backed by locked collateral tokens. MAI borrowing is decentralized and non-custodial. MAI can only be made through locking collateral to back its value – either through approved collateral in vaults or through swapping other stables. Collateral can be static tokens like LINK, CRV, and others. It can also be exotic assets like Beefy and Yearn strategies. Interest-bearing collateral like Beefy, Yearn, and Aave receipt tokens allow users to accumulate yield from their collateral while it’s deposited in MAI vaults.

To make MAI through vaults, users can deposit collateral in their vaults and mint MAI against it. Users can earn QI token rewards while they hold debt with the protocol. You will not be charged interest for minting MAI through vaults. This means you can hold MAI debt long term without accruing costs, however,there is a .5% repayment fee when users pay off their debt.

RAI ($64 million market cap)

RAI puts an interesting twist on the stablecoin concept by not targeting a specific asset for pegging. Developed by Reflexer Labs, RAI is not pegged to any fiat currency and its monetary policy is managed by an on-chain, autonomous controller. It’s a fork of Maker’s DAI.

Failed Stablecoin Experiments

Basis

The Basis project was meant to be an “algorithmic central bank” that utilized a strategy to buy back Basis tokens when the price dropped below the benchmark peg and create new tokens when the price dropped below the benchmark peg. They had $133 million in funding from major VC funds but had to shut down December 2019 due to pressure from regulators.

Empty Set Dollar

The ESD protocol used a supply rebase mechanism that expanded on the work of Basis.io and the protocol included a novel new mechanism in place of Basis’ seigniorage shares. The novel mechanism failed to keep peg with the US dollar and ESD is currently trading around $.08 rather than a dollar.

EDIT – 5/22 -UST ($16 Billion market cap at peak)

Luna/Terra is a controversial project that gained considerable market share in the last 12 months that led to a catastrophic collapse in May. Terra is a blockchain protocol with several decentralized stablecoin projects running on it, the most popular being TerraUSD (UST). The stablecoin tried to maintain a peg using the LUNA token that uses mint and burn mechanisms along with arbitrage incentives. This was subsequently shown to be a flawed model and UST lost peg and the system printed so much LUNA the price dropped 99% in one day.

Liquidity Pools, Lending Platforms, Farms and Vaults for Stablecoin Yield

After determining which stablecoin projects have an acceptable amount of risk, investors can start looking for yield opportunities with that token. As a general rule, the risker stablecoin projects tend to have higher yields to compensate users for the risk. There are several places to seek out yield for stablecoins. We will start with the base layer of DeFi yield, decentralized exchanges and lending platforms.

Sources of DeFi stablecoin yield

The base layer of DEXes and lending protocols is where “organic” yield is generated. Farms and vaults often generate yield by issuing project tokens which is considered “inorganic” as it is not created by market demand or usage and the value comes from diluting the circulating token holders.

DEXes generate yield by charging traders a fee to swap in and out of tokens and those fees are distributed to liquidity providers meaning the yield is tied to the volume of activity happening on the exchange.

Lending and borrowing platforms generate yield through traders using assets as collateral to borrow other assets they wish to speculate on. The fees from borrowing are used to pay users providing the liquidity.

It is important to note that the projects listed are just a snapshot of the well established or popular players in their respective spaces. There are many different variations and approaches out there.

DEXes and liquidity pools – generating yield via fees from trading activity

DEXes use the AMM model to facilitate onchain transactions. A DEX functions like a centralized exchange in terms of allowing people to trade, but differs from services like Coinbase due to their permissionless nature that allows anyone to trade or provide liquidity to the platform. It can get a little confusing as sometimes DEXes have yield farms and other cases do not offer any token incentives to LP’s.

Uniswap ($30-$60 billion in trading volume per month)

Uniswap was the first DEX to gain popularity with version two of the protocol that utilized a 50/50 AMM model for liquidity providers. It created an easy to use interface for swapping all kinds of exotic ERC-20 tokens. At one time it issued UNI tokens as an incentive, but today relies on yield from swap fees to lure liquidity providers to the platform. Uniswap changed drastically when upgrading to version three, requiring more active management from liquidity providers in contrast to version two which allowed for a more passive approach.

How to Find Stablecoin Liquidity Pools for Yield

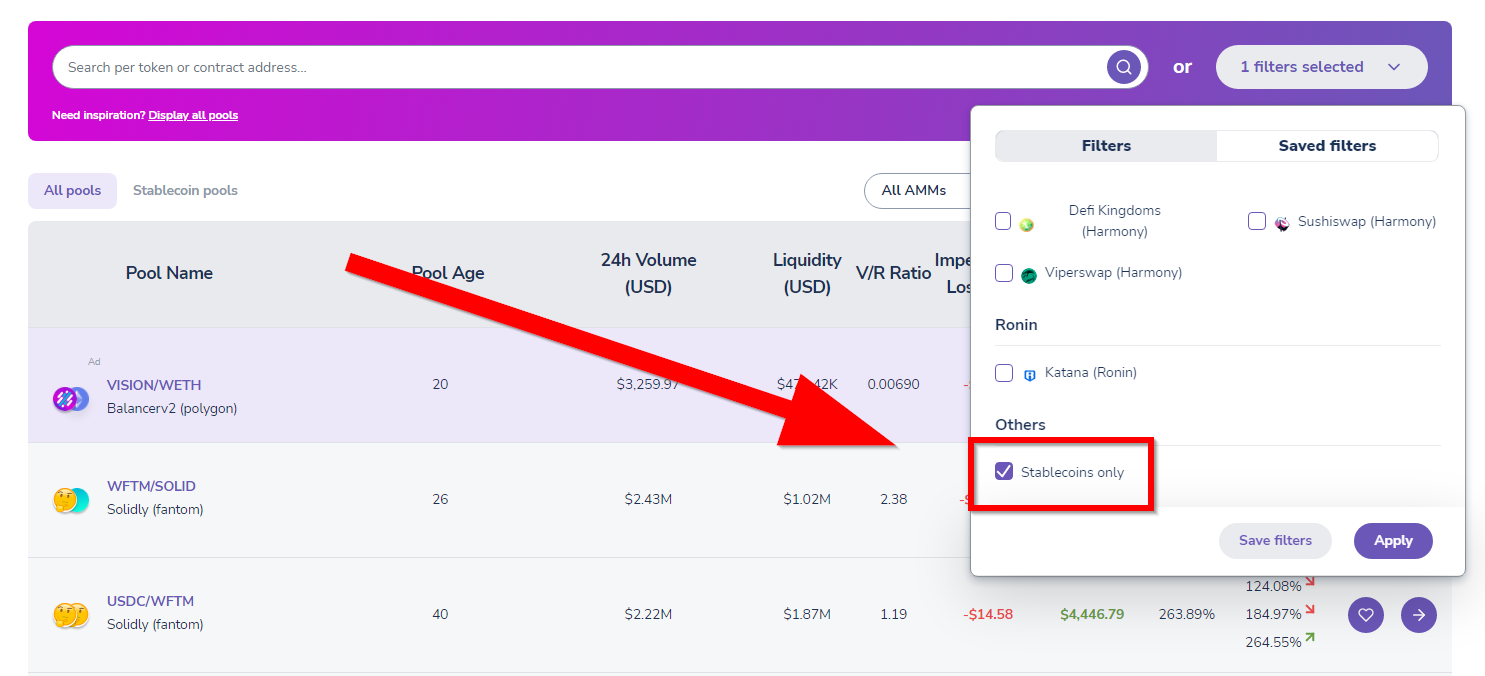

APY.vision has created a tool that makes it easy to find DEX liquidity pools that offer attractive yields. Navigate over to our “Top Performing Pools” page to find a list of all the opportunities to earn stablecoin yield. Once you are there, click the “Filter” option to bring up the menu pictured below.

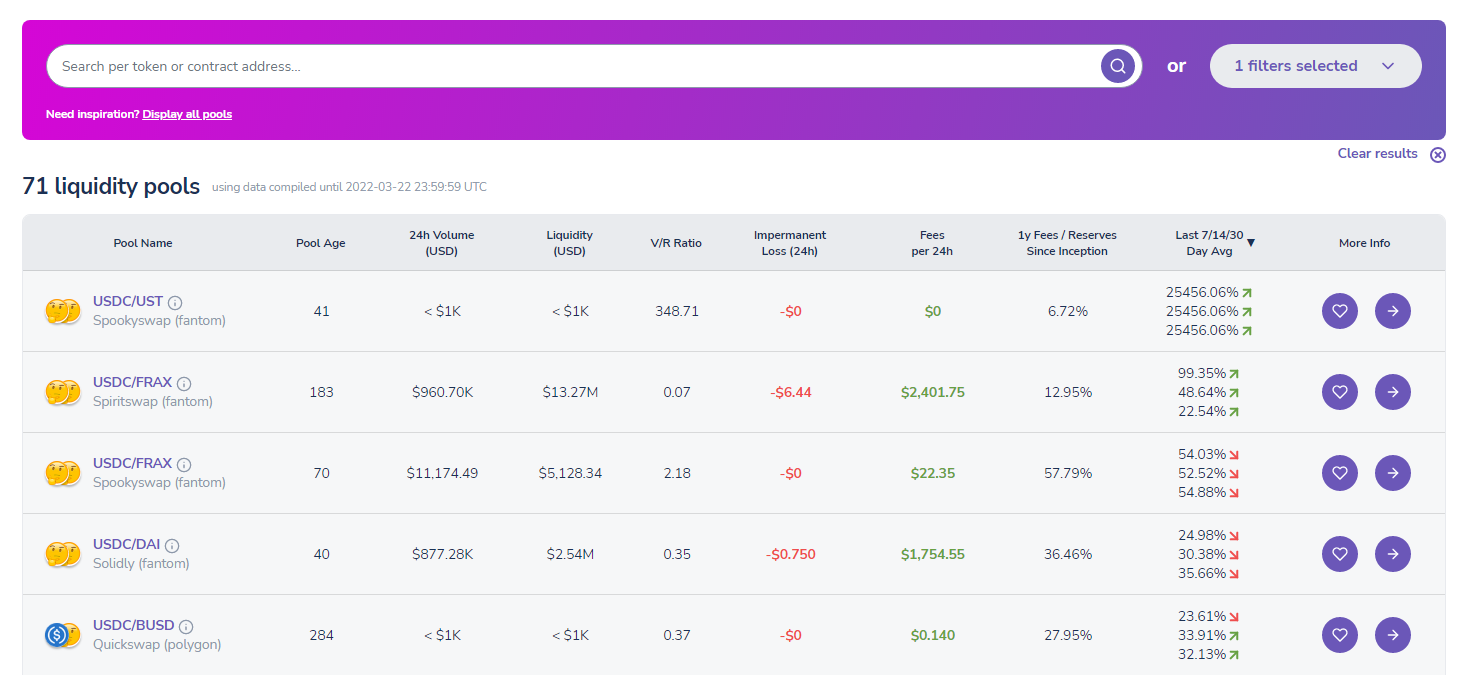

Click the button that says “Apply” to apply the filter and then you will see what is pictured below, a list of all the stablecoin pools on various DEXes and their performance over time. Many of the pools are generating annual yields over 20%!

Lending and Borrowing – generating yield from leveraged speculators

The early DeFi lending protocols such as Compound and Aave are now seen as the standard in the marketplace. These protocols offer lending or borrowing of popular tokens, such as ETH, USDC and others. Any new tokens that want to be included on the platform must be approved by voting through a governance framework before they can be listed.

Aave ($13 billion Total Value Locked)

Aave is the market leader in the lending and borrowing space, distinguishing itself by offering a wide variety of tokens in the protocol and creating innovative features like flash loans.

Compound ($7 billion Total Value Locked)

Compound offers a similar service to Aave but takes a more conservative approach and offers less borrowing power and a smaller number of supported assets.

“Total Value Locked” measures the amount of funds that users have deposited into a protocol. It is not a perfect measurement, but it does signal investor confidence in the safety of a given protocol. A protocol with a low TVL is generally seen as higher risk, especially if the project is new.

Stablecoin Yield Farms – A Secondary Layer on Top of the DEX activity

Yield farms (sometimes called liquidity mining or rewards) are added incentives that DEXes offer to encourage liquidity providers to take on the risk of impermanent loss. This concept was made popular during the rivalry between Uniswap and Sushiswap. SushiSwap forked Uniswap and started issuing the SUSHI token as a reward to liquidity providers, encouraging Uniswap to do an airdrop and rewards program for the UNI token.

Curve ($20 billion Total Value Locked)

Curve is a DEX focused on ultra efficient stablecoin swaps with very low fees and slippage. They also issue the CRV token as a reward to LP’s which is governed by the innovative veCRV model. Users lock their CRV and convert it into veCRV which is used to vote on the future yield farm reward allocations.

SushiSwap ($4 billion Total Value Locked)

SushiSwap was created in 2020 by pseudonymous entities Chef Nomi and 0xMaki. The founding team forked the open-source code of Uniswap to create the basis for SushiSwap.They differ from Uniswap due to their ongoing farm programs that reward SUSHI tokens to liquidity providers.

Balancer ($3 billion Total Value Locked)

Balancer is a DEX that has innovated on the 50/50 AMM model by creating pools that can support up to 8 assets in a variety of different weights to help prevent impermanent loss that is one of the drawbacks of the 50/50 model. They offer their BAL token as an incentive on many of their pools.

Stablecoin Vaults – A Third Layer on Top of the Farm

The concept behind vaults is to find a yield farm and then harvest the rewards on behalf of the users and auto compound them to batch gas costs and increase the long term yield. Vaults can take different approaches but the general idea is to make the investment require less management from the user.

Yearn ($3 billion Total Value Locked)

Yearn was the original vault product and focuses on simplicity for the user. One asset is deposited into a vault and then the vault employs a strategy to use that liquidity to find yield and distribute it back to the pool of funds in the vault.

Beefy ($900 million Total Value Locked)

Beefy is a multichain yield aggregator that takes advantage of various farming opportunities for their vaults and provides an auto compounding service for the user. They commonly take LP tokens from DEXes as deposits into their vaults.

Conclusion

In situations where traders believe there is a bear market coming, trading risky assets for stablecoins and finding a place for them to earn some yield is an intelligent strategy. Having that cash ready to “buy the dip” is a great place to be!

APY.Vision does not give investment advice and always insists that you do your own research. Read our full Legal Disclaimer.

Check out APY.Vision!

APY.Vision is an advanced analytics tool for liquidity pool providers and yield farmers. If you’re using any DEXs, AMMs, or liquidity pools this is the tool you will need to easily track the ROI of your liquidity provider and yield farming activities. Try it now!